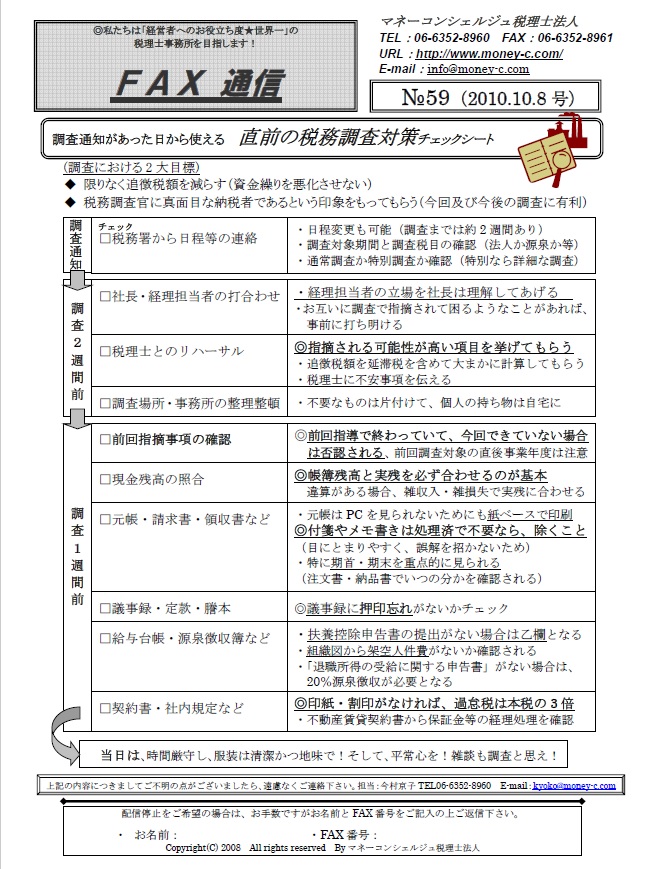

카톡상담

카톡상담Improving Tax Compliance or Understanding Tax Audits and Penalty Waive…

페이지 정보

작성자 Lacey Makowski 댓글 0건 조회 15회 작성일 25-05-13 22:47본문

There are several types of tax audits, including mail audits, office audits, and field audits. Correspondence audits are typically conducted by mail and involve the exchange of information between the taxpayer and the tax authority. Office audits are conducted at a tax authority's office and may involve a face-to-face meeting between the taxpayer and a tax auditor. Field audits are typically more in-depth and may involve a visit to the taxpayer's place of business or residence.

During a tax audit, a tax auditor may request additional information or documentation to support the taxpayer's tax claims. The taxpayer is obligated to work with the tax examiner and provide the requested information in a timely manner. Failure to comply with a tax audit request may result in penalties and fines.

In some cases, taxpayers may be subject to a penalty or fine if they are found to have underreported income, claimed excessive deductions, or failed to file tax returns on time. However, taxpayers who cooperate with tax authorities during an audit and demonstrate a willingness to comply may be eligible for penalty abatement.

Penalty abatement is a process by which taxpayers can request that the tax authority reduce penalties and fines associated with tax noncompliance. To qualify for penalty abatement, taxpayers typically must demonstrate that they were unaware of any errors or omissions.

Taxpayers who wish to pursue penalty abatement should gather all relevant documentation and information, including supporting evidence, 税務調査 事前通知 financial statements, and correspondence with the tax authority. They should also submit a paper request to the tax authority, explaining the reasons for the noncompliance and demonstrating a willingness to comply.

The tax authority will review the taxpayer's request and may request additional information or documentation before making a decision. The decision to waive penalties and fines is typically made on a case-by-case basis and is subject to the tax authority's discretion.

In some cases, taxpayers may be eligible for automatic penalty abatement due to circumstances such as the tax authority's own error. Taxpayers who meet these criteria may not need to submit a separate request for penalty abatement, but should still collect supporting documentation to demonstrate their eligibility.

Ultimately, taxpayers who are subject to a tax audit or penalty should seek the advice of a expert tax professional. A tax professional can help taxpayers understand their obligations, identify potential issues, and navigate the tax audit and penalty abatement process. By cooperating with the tax authority, taxpayers may be able to limit their liability and avoid unnecessary civil penalties.

- 이전글서울 구로구 약물중절수술병원 (산부인과미프진처방비용) 약물유산미프진낙태확률 25.05.13

- 다음글4 Guilt Free Highstakes Online Casino Tips 25.05.13

댓글목록

등록된 댓글이 없습니다.